2024 Forein Student Test/Retest Questions – Answers:

2024 Foreing Student Test Pass 96% Proof:

Residency Status, Form 8843, and Filing Status – Test Questions:

2024 Foreing Student Pass 96% Proof:This section of the VITA/TCE certification Foreign Student test covers determining residency status, the use of Form 8843, and filing status. It consists of 13 true/false questions.

1. Maylor entered the U.S. on July 30, 2021 as a student in F-1 immigration status. He had never been to the United States before and he did not change immigration status during 2024. For 2024 federal income tax purposes, Maylor is a resident alien.

a. True

b. False Answer

2. Amelia is a visiting professor at the local university. Amelia was a graduate student from June 2020 to May 2022 in F-1 immigration status. She re-entered the United States as a teacher on December 20, 2023 in J-1 immigration status. For 2024 federal income tax purposes, Amelia is a ________.

a. Nonresident alien

b. Resident alien Answer

3. Lucas was a student in F-1 immigration status from December 2015 through June 2023. In August of 2024, Lucas returned to the United States as a graduate student. For 2024 federal income tax purposes, Lucas is a ________.

a. Resident alien Answer

b. Nonresident alien

4. Antonio came to the United States in F-2 immigration status with his wife on July 15, 2020. He has not changed his immigration status. For 2024 federal income tax purposes, Antonio is a ________.

a. Resident alien

b. Nonresident alien Answer

5. Anne was in the U.S. as a child in J-2 immigration status with her parents from 2012 through 2015. She re-entered the U.S. in 2023 as a student in J-1 immigration status. The time she was present in the U.S. as a child is considered when determining her total number of years with exempt days.

a. True Answer

b. False

6. Janice entered the United States on August 1, 2020 in J-1 student immigration status. On August 10, 2023, her husband Rick joined her in J-2 immigration status. Janice and Rick had no income in 2024.

Are Janice and Rick required to file any form(s)?

a. Yes, Form 8843 Answer

b. No, no forms required

c. Yes, 1040NR and Forms 8843

d. Yes, 1040 filing married filing jointly

7. Janice and Rick from Question 6 have twins prior to entering the US. For 2024, how many Form(s) 8843 does Janice's family need to file?

a. 1

b. 2

c. 3

d. 4 Answer

8. Jocelyn and Connor have been in the U.S. in F-1 immigration status, since July, 2018. Their 12-year old daughter Arya, has been attending boarding school since June, 2017 on F-1 immigration status. For 2024, who must file Form 8843?

a. Arya

b. All three of them

c. None of them Answer

d. Jocelyn and Connor

9. Ayesha is from Pakistan and is a Ph.D. student in cyber security who is going to defend her dissertation in June 2025. She arrived in the U.S. as a student in F-1 immigration status on June 30, 2021. For 2024 federal income tax purposes, is Ayesha a nonresident alien?

a. Yes Answer

b. No

10. Klaus is a junior majoring in marine biology. He is in the U.S. as a student in F-1 immigration status from Germany. He transferred from a German university and arrived in the U.S. on April 15, 2021. Klaus worked in a lab on campus and as a summer intern for a company in New York. He will graduate in May 2025. For tax purposes, Klaus is considered a ___________.

a. Resident alien

b. Nonresident alien Answer

11. Cyriltavo is a nursing student from Greece who first arrived in F-1 immigration status on August 15, 2024. He did not work or receive a scholarship in 2024, but had $100 interest income from his U.S. savings account his parents set up for him to pay for school and his living expenses. Cyriltavo must file Form 1040-NR for 2024.

a. True

b. False Answer

12. Orlando entered the U.S. in J-1 immigration status as a trainee in January 2023 and lives alone. His wife, Bey, could not accompany due to on-going health concerns. Orlando must file as a______________ even though his spouse was not present in the U.S.

a. Single

b. Qualifying Surviving Spouse (QSS)

c. Married Filing Separately (MFS) Answerr

13. Tomas and Olga were married in March 2020. The next year, they both entered the U.S. in F-1 immigration status to complete their studies as Fulbright scholars. Currently, Tomas lives in San Diego where he is completing his graduate work. However, Olga left him in March 2024 and has not been heard from since. Her parents will not tell him where she lives. Although Tomas does not know Olga's whereabouts, he still must file as Married Filing Separately (MFS).

a. True Answer

b. False

2024 Foreign Student Scenario 1 Gabriel Alvarez – Interview Notes and 4 Questions:

Use the following information to prepare Form 8843.• Gabriel Alvarez came to the U.S. to study on August 1, 2021, in F-1 immigration status. His passport number is 4682936 and it was issued by his home country, Peru. His home address is 31 Rue de Santos, Lima, 07001, Peru. His address at school is Stanford University, 450 Jane Stanford Way, Stanford, CA 94305. His U.S. taxpayer identification number is XXX-XX-XXXX.

• Gabriel is attending Stanford University, 450 Jane Stanford Way, Stanford, CA 94305, telephone 612-555-XXXX. His specialized program is Alternative Fuel Systems and the director is Professor Marri M. Young, also at 450 Jane Stanford Way, Stanford, CA 94, telephone 612-555-XXXX ext. 1267.

• Gabriel has not taken steps to apply for permanent residency. Gabriel had no income, so he is not required to file any other tax forms. Gabriel has not left the U.S. since arriving.

• After completing the required tax form, review the scenario and resource materials, and answer each of the test questions.

To answer the following multiple choice questions, refer to the Form 8843 you completed for Gabriel Alvarez.

14. Gabriel reports his most current nonimmigrant status on line 1a.

a. True

b. False Answer

15. Gabriel should put 365 days on line 4b, for days of exempted presence for 2024.

a. True Answer

b. False

16. What parts of Form 8843 does Gabriel need to complete?

a. Part I

b. Parts I and III Answer

c. Parts I and II

d. Part II

17. Gabriel must submit his Form 8843 for tax year 2024 by April 15, 2025?

a. True

b. False Answer

Taxability of Income, ITINs, and Credits – 7 Test Questions:

Introduction:This segment of the VITA/TCE certification test includes 7 questions on taxability of income, ITINs, and credits.

18. Jenna, who is a nonresident alien and is in the United States in J-1 immigration status, spent $4,400 on qualifying education expenses. She is eligible to claim an education credit on her tax return.

a. True

b. False Answer

19. Lacey received $100 of dividend income on U.S. stocks she purchased online. She is an international student from Canada in F-1 immigration status. She arrived in the United States in 2023. How much of Lacey's dividend income will be taxed at 30%?

a. $0, it's taxed at the ordinary rate

b. $0, Per Publication 4011, the correct tax rate is 15% Answer

c. $100

20. Tonya and Paul are a married nonresident alien couple from France. Both are in the U.S. in F-1 immigration statuses and arrived in 2024. They paid $3,700 in childcare expenses, while attending school, for their child who was born in the United States and is a U.S. citizen. They are eligible to claim the child and dependent care credit on their Form 1040-NR.

a. True

b. False Answer

21. Jaden is a student in J-1 immigration status from Latvia. He earned $2,300 in wages in 2024. His wages are reported to him on Form 1042-S (Box 1, Income Code 20). Should Jaden report his wages on Form 1040-NR, Schedule OI?

a. Yes Answer

b. No

22. Cyril is a student in the U.S. in J-1 immigration status as of October 15, 2024. Under the terms of his visa, he is permitted to work in the U.S. Cyril qualifies for a Social Security number and should not apply for an ITIN.

a. True Answer

b. False

23. Mihaela, a student in F-1 immigration status from Slovenia, is on the tennis team. Mihaela arrived in the U.S. on July 20, 2024 on a full athletic scholarship that includes $8,000 for room and board and $28,000 for tuition and fees. What amount will be taxable on Mihaela Form 1040-NR?

a. $36,000r

b. $28,000

c. $8,000

d. $0.00 Answer

24. Stefan is a student in the U.S. in F-1 immigration status. Stefan arrived from Germany on August 5, 2022. Stefan worked in the bookstore and earned $3,200 in wages and had federal income tax withholding of $330. Stefan is only required to file Form 8843 for 2024.

a. True

b. False Answer

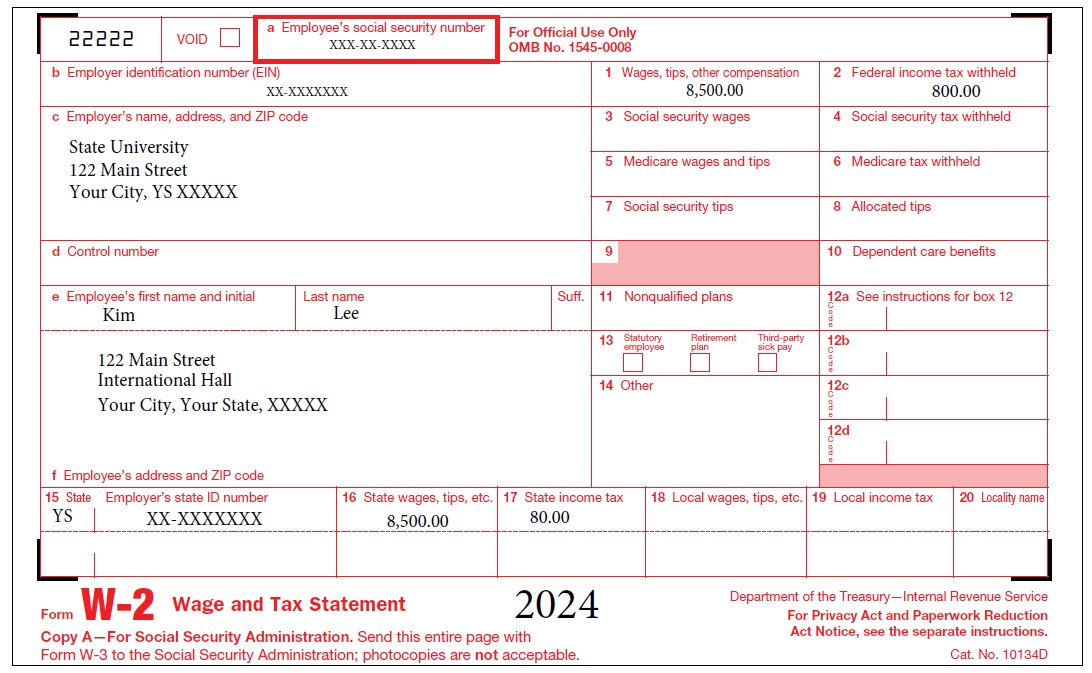

2024 Foreign Student Scenario 2 Kim Lee Interview Notes – 5 Test Questions:

Use the following information to prepare Form 1040-NR.• Kim Lee, a citizen of South Korea, came to the United States in F-1 immigration status (number 3344123344) on January 01, 2024.

• He has remained in the country since then and is a full-time student at the local university. Kim, born July 25, 2001, is single. He began working at the university on February 10, 2024.

• He filed the proper withholding and treaty forms with the university payroll office before beginning his job. Since filing these forms correctly, he received a Form 1042-S for the treaty benefit for his wages. Kim was not in the U.S. before and therefore, has not filed an U.S. tax return in any prior year.

• Kim also received a scholarship from the university he was attending. He filed the appropriate forms to claim his treaty benefit for the scholarship. Therefore, he received a Form 1042-S.

• Kim’s address in South Korea is Bldg. 102 Unit 304, Sajik-ro-3-gil (Street) 23, Jongno, Seoul (South Korea) 30174. If he is entitled to a refund, he wants a direct deposit to his checking account. The routing number is 123456789 and the account number is 98765432100. He doesn’t want to designate anyone to discuss his return with the IRS. He did not take any affirmative steps to apply for permanent residence in the U.S. Kim’s U.S. income will not be taxed in his home country.

• Using the following information (two Forms 1042-S and a Form W-2), complete Kim’s federal income tax return. (Kim would also need to file Form 8843, but assume that he has already completed that on his own.)

• After completing the required tax form, review the scenario and resource materials, and answer each of the test questions.

2024 Foreign Student Scenario 2 Kim Lee – 5 Test Questions:

Directions: To answer the following multiple choice questions, refer to the Form 1040-NR you completed for Kim Lee.25. Is $8,500 the amount entered on the line for Total amount from Form(s) W-2, box 1 on Form 1040-NR?

a. Yes Answer

b. No

26. Is $8,500 the amount of adjusted gross income on the Form 1040-NR?

a. Yes Answer

b. No

27. What is the amount of Itemized deductions on the Form 1040-NR?

a. $0.00

b. $80 Answer

c. $800

d. $880

28. Is $8,420 the amount for taxable income on the Form 1040-NR?

a. Yes Answer

b. No

29. What is the total amount entered for Total income exempt by a treaty from Schedule OI?

a. $0

b. $2,000

c. $6,000

d. $8,000 Answer

Solution to Question 29:

Form 1042-S Income Code 20:

Korea South – Treaty Benefits for Studying Income Code 20: Max Years in U.S. 5 and Max Dollar Amounts $2000.

Form 1042-S Income Code 16:

Korea South – Treaty Benefits for Scholarship Grants Income Code 16: Max Years in U.S. 5 and Max Dollar Amounts No Limits.

Total income exempt by a treaty from Schedule OI is $2000 + $6000 = $8,000.

2024 Foreign Student Scenario 3 Amar Pavan – Interview Notes:

Use the following information to prepare Form 1040-NR.• Amar Pavan, a citizen of India, came to the United States as a student. He entered in F-1 immigration status (visa number 88779914) on September 1, 2021. He has remained in the country since then and is a full-time student at the local university.

• Amar was born on July 30, 2000, and is single. He filed the proper treaty and withholding forms with the university payroll office. Amar has filed a U.S. tax return Form 1040-NR for 2023. His address in India is B block, GK II, New Delhi – South, Delhi NCR, India.

• If he is entitled to a refund, he wants it mailed to him. He doesn’t want to designate anyone else to discuss his return with the IRS. Amar has not taken any steps to apply for permanent residence in the U.S.

• He will not be taxed in his home country on the income he has from the U.S. Using the following Form W-2, prepare Amar’s federal income tax return. (He has already completed his Form 8843.)

• Amar received $25 in bank interest from an account he opened with money from his parents, this money is not connected with a U.S. trade or business.

• He owed additional State Income tax when he filed his taxes last year. He mailed a payment of $85 on April 1, 2024 to his state.

• He donated $200 to the American Red Cross as a charitable contribution.

• He also donated $1,000 cash to his church but has no record.

• After completing the required tax form, review the scenario and resource materials, and answer each of the test questions.

2024 Foreign Student Scenario 3 Amar Pavan – 4 Test Questions:

Directions:To answer the following questions, refer to the Form 1040-NR you completed for Amar Pavan.

30. What is the Adjusted Gross Income (AGI) on Form 1040-NR?

a. $12,400

b. $25,800

c. $27,000 Answer

d. $27,025

31. Amar Pavan is a student who is considered a resident of India. According to the U.S.-India Tax Treaty, he can take the standard deduction instead of itemizing.

a. True Answer

b. False

Solution to Question 31:

Yes, an international student from India studying in the US on an F, J, or M visa can generally take the standard deduction on their U.S. income tax return.

32. Amar will have a refund on Form 1040-NR?

a. True Answer

b. False

33. The taxable income line on Amar’s Form 1040-NR shows $25,800.

a. True

b. False Answer

2024 Foreign Student Scenario 4 Sonya Ivanov – Interview Notes and 4 Test Questions:

Use the following information to prepare 2024 Form 1040-NR.• Sonya Ivanov is a resident of Bulgaria (visa number 38755219). She arrived in the United States in F-1 immigration status on September 1, 2022 as a full-time student. Sonya is 25 years old, single, born on July 11, 1998. Her address in Bulgaria is Vna 74117 Varna, Grand Mol Varna, 9021 Bulgaria.

• Sonya has not taken any steps to apply for permanent residence in the United States. Sonya did not file a Form 1040-NR in 2023 as she did not work that year. She started a new job with the university bookstore on January 20, 2024.

• If she is entitled to a refund, she wants a direct deposit to her checking account. The routing number is 789654321 and the account number is 011233456789. She will not be taxed by the Bulgarian government on the income she has earned in the United States. Assume Sonya has already completed her Form 8843, and prepare her federal income tax return with the following Form W-2. College Town University reports all student income on Form W-2. Miss Ivanov failed to respond to the university in time for them to properly issue Form 1042-S for her treaty-exempt income. However, she is still entitled to take her treaty benefit on her tax return instead.

• After completing the required tax form, review the scenario and resource materials, and answer each of the test questions.

2024 Foreign Student Scenario 4 Sonya Ivanov – 4 Test Questions:

Directions:To answer the following multiple choice questions, refer to the Form 1040-NR you completed for Sonya Ivanov.

34. Sonya is allowed to exclude all of her wages as a treaty benefit on Schedule OI?

a. True

b. False Answer

Solution for Question 34:

No, the IRS does not allow a complete exclusion of all wages as a Bulgaria treaty benefit.

While the US-Bulgaria income tax treaty offers some benefits to residents of Bulgaria working in the US, it does not provide a complete exclusion of all wages from US taxation for nonresident aliens.

35. The total amount of the W-2, box 1, wages, salaries, tips, is reported on the Total amount from Form(s) W-2, box 1 line of the Form 1040-NR.

a. True Answer

b. False

36. Form 1040-NR, schedule OI, line G shows Sonya's treaty benefit information.

a. True

b. False Answer

Solution for Question 36:

Schedule OI (Form 1040-NR) is used by nonresident aliens to provide additional information not directly entered on Form 1040-NR. This includes details about claiming benefits under a tax treaty, specifically on line G.

37. Sonya's itemized deductions is $0.00?

a. True

b. False Answer

2024 Foreign Student Refunds, Deductions, and the Best Form to Use – 13 Test Questions:

Introduction:This part of the VITA/TCE certification test includes 13 true/false or multiple choice questions.

Allow approximately 20 minutes to complete this segment.

38. Erin, an international student from Ireland, has a Form W-2 that shows amounts withheld for Social Security and Medicare taxes. Erin is an F-1 student who first arrived in the U.S. in 2020. Can she file Form 843 to receive a refund of these taxes?

a. True Answer

b. False

Solution to Question 38:

Refunds of Social Security and Medicare Taxes erroneously withheld file Form 843 to claim refund. 39. Jorge and Marta are from Mexico. Jorge is a scholar at a local university in J-1 immigration status and Marta is in J-2 immigration status. Marta worked at a local boutique in 2024. Her Form W-2 shows Social Security and Medicare tax withholding, while Jorge's does not. Marta is entitled to the exclusion of Social Security and Medicare tax withholding as a spouse.

a. True

b. False Answer

Solution to Question 39:

Individuals in F-2 or J-2 immigration status are never exempt from FICA (Social Security and Medicare Taxes).

40. Li, an international student from People's Republic of China, received $10,100 of interest income in 2024 from a personal bank account in the U.S. he opened when he first arrived on August 27, 2021. He also had a $100 capital gain from some U.S. stock he sold. Li reports the stock sale on Schedule D.

a. True

b. False Answer

41. Jackson entered the United States for the first time in 2022. He is a resident of France and is in F-1 immigration status. Jackson won $1,200 at the local casino. Jackson will report the $1,200 on Schedule NEC.

a. True Answer

b. False

42. Maylor is a visiting scholar from Ireland. He arrived in the U.S. on September 1, 2023 in J-1 immigration status and was accompanied by his wife and son. They had a second child in 2024, born in the U.S. Maylor is required to file a federal income tax return. When he files his federal tax return, he cannot claim his wife and children as dependents.

a. True Answer

b. False

Solution to Question 42:

It's unlikely a visiting scholar from Ireland on a J-1 visa can claim a child born in the U.S. as a dependent on their U.S. tax return, unless the child is a U.S. citizen or resident alien.

43. Gilberto, a graduate student from Germany, is in F-1 immigration status. He has been here since April 1, 2024. He has receipts for his donations to his church in Germany as well as donations made to a U.S. charity. Gilberto can claim all his charitable contributions as an itemized deduction on Form 1040-NR.

a. True

b. False Answer

44. Aretha is in F-1 immigration status from Chile. She entered the United States in August 2020 and enrolled as a full-time undergraduate student. Aretha is pursuing her first degree in mathematics. Aretha qualifies for the American opportunity credit.

a. True

b. False Answer

45. Jenna is a single, nonresident alien who began studying in the U.S. in 2020 in F-1 immigration status from Ecuador. She has wages of $9,300, interest income from her savings account of $175, $50 of dividends, and sold $4,500 of U.S. stocks for a $250 capital gain. She donated $50 of the proceeds to a local charity. Jenna cannot have her return prepared at any Foreign Student and Scholar VITA site, because she has capital gain income.

a. True

b. False Answer

Solution to Question 45:

IRS Volunteer Income Tax Assistance (VITA) program can help taxpayers with reporting capital gains and losses from the sale of stock.

46. Some students and scholars may owe money with their tax return. Generally, nonresidents have the option to set up an installment agreement.

a. True Answer

b. False

47. Dmitry, who is from Russia, earned wages of $12,335 in 2023. He had $280 withheld for state income taxes. He listed the state taxes as a deduction on his federal tax return in 2023 which lowered his taxable income. Dmitry received a state refund of $200 in 2024 from the 2023 tax return. Will Dmitry report his state tax refund as income on his Form 1040-NR in 2024 or amend his 2023 return?

a. He needs to include the state income tax refund on his 2024 federal return. Answer

b. He will remove the $125 state taxes from his 2023 deductions with an amended return.

c. He does not need to do anything with his state income tax refund.

48. Brunilda came to the U.S. in 2022 for postgraduate study. She took out a student loan to help pay the tuition through her school’s financial aid office. Brunilda graduated in December 2023 but remained in the U.S. for one year of practical training. She began repaying the loan on August 1, 2024 and paid $65 in interest during 2024. Where can Brunilda claim this interest?

a. Itemized deduction

b. Credit

c. Adjustment to income Answer

d. None of the above

Solution to Question 48:

From Schedule 1 (Form 1040) line 21 Student loan interest deduction and Form 1040-NR line 10 Adjustments to income from Schedule 1 (Form 1040), line 26. These are your total adjustments to income.

49. Matteo, a student from Malta, had $8,500 in wages reported to him on Form W-2. Although all of his wages are excluded from tax by treaty, he is required to file a tax return.

a. True Answer

b. False

50. Mustafa is a resident of Egypt attending college in the U.S. He arrived on J-1 immigration status in June of 2024. He had $15,800 in wages reported on Form W-2 and $39 in dividend income. Mustafa must complete both Schedules OI and NEC with his Form 1040-NR.

a. True Answer

b. False